If you’ve been following the “variance analysis” series, then you’ve already learnt how to calculate the following:

So far, all the calculations we’ve been doing show us variances between actual and budget. These are known as operational variances. For today, we shall try our hand at something easy – planning variances.

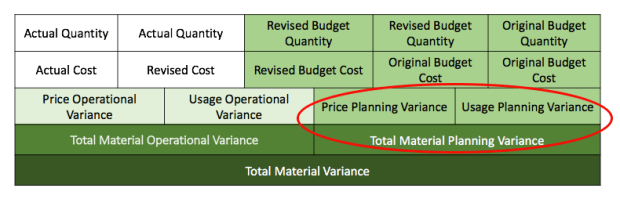

Planning variances are derived from comparing our original budget to revised budget figures. Planning variances showcase the talent and skill of managers in forecasting changes in either prices or capacity. These planning variances would normally be within the control of the managers and can be identified way in advance (time-wise).

Let’s get back to our visual illustration for the past few weeks but let’s tweak it a bit to accommodate planning variances.

Example information: Original budget output was 600 units. Original budget input per unit of output was 0.5kgs. Original standard cost was £10 each kg. Revised budget input per unit of output was 0.75kgs. Revised standard cost was £9 each kg. Calculate the planning variances and differentiate.

So let’s do the calculations as follows:

Calc 1: Output of 600 units x revised budget input of 0.75kgs per kg = 450kgs. 450kgs x revised standard cost at £9 = £4050

Calc 2: Output of 600 units x revised budget input of 0.75kgs = 450kgs. 450kgs x original standard cost at £10 = £4500

Calc 3: Output of 600 units x original budget input of 0.5kgs = 300kgs. 300kgs x original standard cost at £10 = £3000

The difference between Calculations 1 and 3 results in a £1050 difference. This difference is known as material planning variance. This is an unfavourable variance because the revised amount will cost us more than what we originally budgeted for.

The difference between Calculations 1 and 2 gives us a favourable £450 difference. The deviation between the original standard cost to the revised cost highlights the material price planning variance.

The difference between Calculations 2 and 3 provides us an unfavourable £1500 difference. The discrepancy between the original budget quantity to the revised quantity points out the material usage planning variance.

These planning variance calculation would also work with labour planning variance, which can be split between labour price planning variance and labour efficiency planning variance. Shall we try an example?

Example information: Original budget output was 600 units. Original production hours input per unit of output was 2 hours. Original standard labour rate was £8/hr. Revised budget production hours input per unit of output was 1.5 hours. Revised standard labour rate increased to £8.25/hr. Calculate the planning variances and differentiate.

So let’s do the calculations as follows:

Calc 1: Output of 600 units x revised hours input of 1.5 hrs/kg = 900 hrs. 900 hrs x revised labour rate at £8.25 = £7425

Calc 2: Output of 600 units x revised budget hours input of 1.5 hrs/kg = 900 hrs. 900 hrs x original labour rate at £8 = £7200

Calc 3: Output of 600 units x original budget hours input of 2 hrs/kg = 1200 hrs. 1200 hrs x original labour rate at £8 = £9600

The difference between Calculations 1 and 3 results in a £2175 difference. This difference is known as labour planning variance. This is a favourable variance because the revised amount will cost us less than what we originally budgeted for.

The difference between Calculations 1 and 2 gives us an unfavourable £225 difference. The deviation between the original labour rate to the revised rate highlights the labour rate planning variance.

The difference between Calculations 2 and 3 provides us a favourable £2400 difference. The discrepancy between the original budget production hours input to the revised one points out the labour efficiency planning variance.

With all these talks of variances, why not nab yourself a copy of Astranti’s P1 study text. And if P1 isn’t your cup of tea at the moment, why not check out the rest that’s on offer?

Please help – I’ve got a recent BPP and Kaplan book that are using REVISED standard costs to value material and labour efficiency variances ( e.g. when the number of hours per unit has been revised the comparison between actual hours and revised hours is measured at new standard cost per hour. This is different in your example above.

I realise there are a few acceptable ways to calculate these variances but CIMA exams will only have one box to input one answer? 😦

LikeLike

Hi CathyShi, the blog piece that you are referring to deals with planning variances. I believe you are looking for operational variances in your question above. May I direct you to my other blog articles, Variance Analysis – Parts 1 & 2?

LikeLike